By Harsh Chauhan

Artificial intelligence (AI) stocks continue to post outstanding

revenue and earnings growth quarter after quarter, but stock prices in

the sector have been under pressure of late due to an array of

macroeconomic and geopolitical factors. Investors, therefore, can now

buy some top AI stocks

at really attractive valuations, as the strong top- and bottom-line

growth that they have been achieving has not yet been fully factored

into their prices.

If you have $1,000 in investible cash right now, I'd suggest putting that money into Micron Technology (MU) and CoreWeave (CRWV ).

Both stocks are trading at extremely attractive valuations, and they

could increase your investment by at least fivefold in the next couple

of years.

Image source: Getty Images.

Image source: Getty Images.

Micron's red-hot growth isn't getting much love from the market

Micron Technology has made its shareholders significantly richer over

the past year, and it can keep doing so, as its latest quarterly

results show. The memory specialist reported blowout numbers for its

fiscal Q2 2026 on March 18, annihilating Wall Street's expectations.

Management also offered phenomenal guidance for the current quarter.

However, Micron's stock

has retreated 30% since it delivered that quarterly report. Concerns

about management's increasing capital expenditures (capex) and its

ability to further improve its margins have been headwinds for the

stock, but that's good news for savvy investors looking to buy a

fast-growing company on the cheap.

The stock trades at a sales multiple of 8.2 and just under 20 times

earnings. Its forward earnings multiple of just 7.6 screams "value." For

a company whose revenue almost tripled in the previous quarter and

whose earnings shot up by 682% year over year, those multiples are too

cheap to ignore.

Investors would probably be making a mistake by not buying this

memory stock right now because the commodity it sells is in short

supply, primarily due to high demand from AI data centers. Last year,

Micron peer SK Hynix said it anticipated demand for AI data center

memory chips, known as high-bandwidth memory (HBM), would increase at a

compound annual rate of 30% through 2030.

A single gigabyte (GB) of HBM consumes three times the wafer capacity

that's needed to manufacture 1 GB of the latest generation of

traditional dynamic random access memory (DRAM). So, the strong jump in

HBM demand explains why manufacturers are anticipating that supply will

remain tight for the next three to five years.

As a result, Micron is likely to continue benefiting from favorable

memory pricing, which is why its earnings are expected to surge.

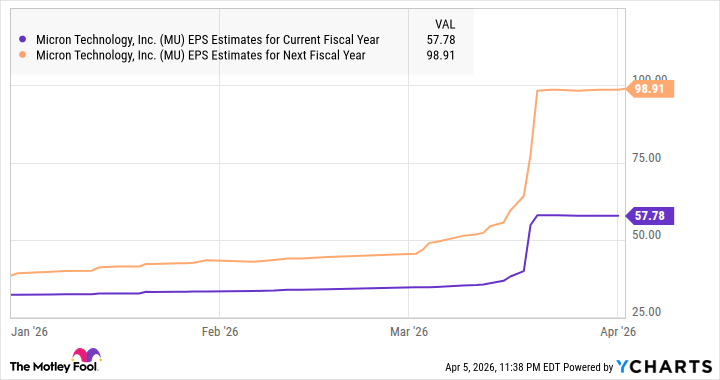

Assuming Micron does achieve $98.91 per share in earnings in the next

fiscal year, and that its forward earnings multiple adjusts to 23 -- in

line with that of the tech-laden Nasdaq 100 index -- its stock price could jump to $2,275. That would be a sixfold jump from current levels.

And as the memory supply deficit is estimated to last until 2030, this semiconductor stock could post even bigger gains by the end of the decade, which is why buying it at its current valuation is a no-brainer.

CoreWeave is a value pick in AI infrastructure

CoreWeave stock is down 39% over the past six months, and trading at

just 7 times sales. That's a very attractive valuation for a company

that is growing its revenues exponentially.

Hyperscalers and AI companies have been using CoreWeave's dedicated

AI data centers to run their workloads. It has huge contracts with the

likes of OpenAI, Meta Platforms, and Microsoft. And it has been diversifying its customer base by adding new customers such as IBM and Mistral AI.

The growing demand for the company's data centers is why it is

aggressively building more. Its capex is poised to jump from $14.9

billion in 2025 to between $30 billion and $35 billion this year. Those

rapidly rising outlays are probably spooking some investors, but those

who are concerned should note that CoreWeave's revenue backlog jumped by

342% year over year in the fourth quarter to $66.8 billion.

Its annual revenue, for comparison, rose 168% to $5.1 billion. Given

that CoreWeave continues to add customers amid growing demand for data

center computing capacity, it needs to aggressively expand its

infrastructure. The company aims to increase its active data center

capacity to 3,100 megawatts by the end of 2027, an almost fourfold jump

from the 850 megawatts it operated last year.

The aggressive expansion explains the rapid growth that analysts expect in the business' top line.

Their consensus forecasts

are for revenue to increase by a multiple of 7 in just three years.

That's why this tech stock deserves a higher price-to-sales multiple.

Currently, it trades at a P/S of 7, a slight discount to the U.S. tech

sector's average multiple of 7.7. But even if CoreWeave is still trading

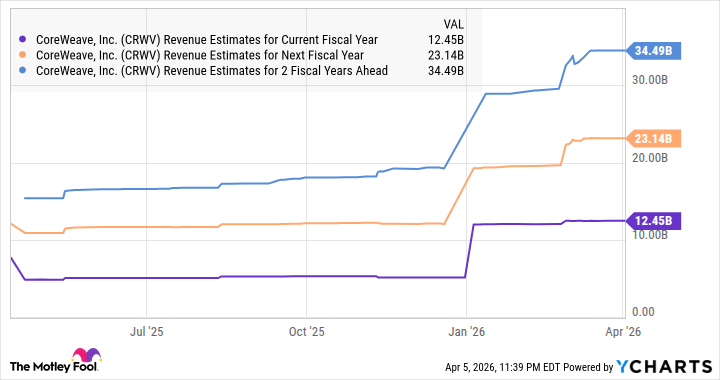

at 7 times sales in 2028, if it achieves $34.5 billion in revenue that

year (as per the chart), its market cap could reach $241.5 billion.

That's almost 5.6 times its current figure. Moreover, CoreWeave stock

could sustain its red-hot momentum beyond the next couple of years

since data center demand is anticipated to remain robust until 2030,

which means investors can buy this potential long-term winner at a

ridiculously cheap valuation right now.

Is CoreWeave a long-term buy right now?

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $536,003!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,116,248!*

Now, it’s worth noting Stock Advisor’s total average return is 946% — a market-crushing outperformance compared to 190% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of April 10, 2026.

Harsh Chauhan

has no position in any of the stocks mentioned. The Motley Fool has

positions in and recommends International Business Machines, Meta

Platforms, Micron Technology, and Microsoft. The Motley Fool has a disclosure policy.

This article was originally published by The Motley Fool