Link copied

Newmont Is Golden: Why Record Gold Prices Make It a Must-Buy Dividend Stock Now.

investing ideas :: 2hrs ago :: source - barchart

By Rich Duprey

Gold prices have climbed to record levels over the past year, turning heads among investors seeking protection against inflation, geopolitical tensions, and currency fluctuations. With spot gold hovering well above $4,500 per ounce in recent months and averaging realized prices that boosted miner margins, the sector delivered standout results in early 2026.

Yet not every gold producer translated those prices into equal gains. Let's examine why Newmont (NEM) stands out—and what its latest earnings reveal about capital allocation in a high-gold-price environment.

Capitalizing on a Golden Opportunity

Newmont, the world's largest gold producer, reported Q1 2026 results, generating a record $3.1 billion in free cash flow, up 12% from the prior quarter, on $3.8 billion in operating cash flow after working capital changes. Attributable gold production reached 1.3 million ounces, with revenue climbing 42% year-over-year (YoY) to $7.31 billion. Adjusted net income hit $3.2 billion, or $2.90 per diluted share. CEO Natascha Viljoen highlighted the performance as keeping the company on track for full-year guidance.

Shares of NEM rose 16% year-to-date, following a strong rally, with the stock trading as low as $94.34 earlier in the period before climbing. Over the trailing 52 weeks, NEM gained 116%. The gold mining sector broadly benefited from elevated prices, but NEM's results positioned it as a leader in converting gold strength into shareholder value. In comparison, the S&P 500 ($SPX) is up just 4.79% in 2026. NEM's gains outpaced the broader market in a period when many equities faced volatility. Smart investors note how gold stocks like NEM often serve as a diversifier when equities wobble.

How Free Cash Flow Powers Shareholder Returns

Free cash flow represents cash left after operating expenses and capital investments. Companies can deploy it in only five ways: pay down debt, pay dividends, fund share buybacks, reinvest in the business, or make acquisitions.

Newmont chose a clear path. It announced an additional $6 billion share repurchase authorization after fully executing its prior program, including $2.4 billion repurchased since the last earnings call. The company also paid a $0.26 per share quarterly dividend. With $8.8 billion in cash on hand and a net cash position of $3.2 billion at quarter-end, Newmont holds ample liquidity for these moves. In short, record FCF from higher gold prices directly funded buybacks that reduce share count and boost per-share metrics.

Those higher gold prices drove the results. Newmont realized an average of $4,900 per ounce in Q1, supporting wide margins. Gold by-product all-in sustaining costs (AISC) fell 21% to $1,029 per ounce—well below full-year guidance—thanks to favorable byproduct credits, productivity gains, and lower sustaining capital. That's a fancy way of saying Newmont kept costs in check while gold prices rose, expanding profitability.

Newmont's Low Costs and Structural Gold Support

Newmont's cost discipline stands out compared to its peers. Low AISC allows the company to generate cash even if gold moderates from recent peaks. Structural factors support elevated prices: central bank buying, persistent inflation concerns, and demand for safe-haven assets remain in place. Gold may not repeat the meteoric rise of the past year, but analysts expect it to hold or climb further amid global uncertainties. That backdrop favors producers with low costs like Newmont.

The gold miner's valuation metrics reflect this strength. NEM trades at a trailing P/E of 12.97 and a forward P/E around 12.5. The PEG ratio sits at 0.85, price/sales at 5.29, and price/book at 3.55. These figures suggest the market prices in solid but not excessive growth expectations relative to earnings power at current gold levels.

That said, risks exist. Newmont faces ongoing operational challenges, including weather impacts at sites like Boddington and potential delays at other assets. Production guidance for 2026 stands at approximately 5.26 million attributable ounces, a planned step-down due to mine sequencing—a trough year before the expected rebound in 2027. Ghana tax changes could add pressure to costs. Investors should monitor execution here, as any slippage could affect margins despite gold's support.

www.barchart.com

www.barchart.com

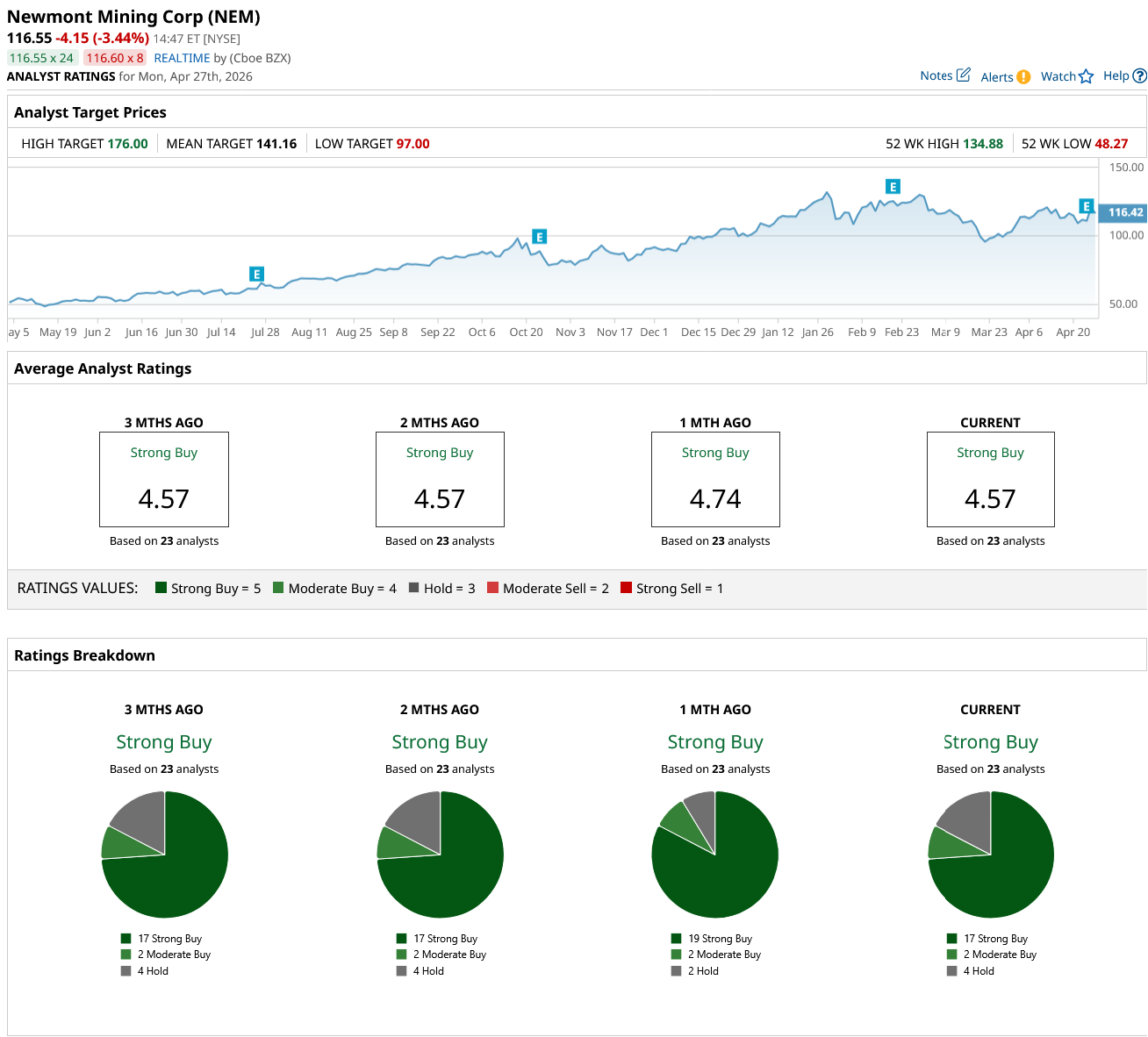

What Analysts Think About NEM Stock

NEM stock maintains a consensus "Strong Buy" rating from 23 analysts. There are 17 "Strong Buy" ratings, two "Moderate Buys," and four "Hold" ratings. The mean price target of $141.16 implies 17% potential upside from around $120, with high targets reaching $176 and lows near $97. That range points to 47% potential upside at the high end, though downside exists if gold pulls back sharply or operations falter. Analysts generally see Newmont as a core holding in the sector.

Bottom Line

Newmont delivered its highest quarterly profits ever through disciplined operations and the gold price tailwind. The $6 billion buyback plan, paired with low costs and a strong balance sheet, signals confidence in returning capital. Gold's structural support suggests prices will likely stay elevated, rewarding efficient producers. Risks around production and specific assets warrant watching, but in a well-diversified portfolio, NEM offers exposure to gold without the volatility of smaller miners.

Granted, no stock is without challenges. Regardless of how you view near-term gold moves, Newmont's FCF generation and capital returns provide a data-backed case for inclusion. Savvy investors may view current levels as an opportunity to own a leader that turns high gold prices into tangible shareholder value.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

This article was first published on Barchart

More News from Barchart

Newmont Is Golden: Why Record Gold Prices Make It a Must-Buy Dividend Stock Now

The 3 Dividend Aristocrats Wall Street Calls a ‘Strong Buy’ With Up to 46% Upside

Upcoming Foldable iPhones Make These 2 Chip Stocks a Buy Now, According to Barclays

3 Under-the-Radar Dividend Stocks Yielding Up to 13% That Wall Street Rates a Strong Buy

This week top market trends.

-

Global equity fund inflows surge to 17-month high on AI optimism

2026-04-24 :: stock :: reuters -

Hedge fund stock buying hits $86 billion as Iran peace hopes, Goldman data shows

2026-04-17 :: stock :: reuters -

Oil prices crater after Trump announces two-week ceasefire in US-Iran war

2026-04-08 :: commodities :: yahoo finance

Recent global market news

-

Here's How Much Dividend Income You'd Have Collected If You'd Bought 100 Shares of Coca-Cola 10 Years Ago

2026-04-22 :: :: motley fool -

Costco (COST) Approves Quarterly Dividend Increase Amid Robust Sales Growth

2026-04-23 :: :: insider monkey