Link copied

This Hidden Growth Story in Taiwan Semi Could Cause TSM Stock to Skyrocket.

trade ideas :: 5hrs ago :: source - barchart

By Jabran Kundi

Taiwan Semiconductor (TSM) is the leading chip manufacturer in the world. The company has some of the top chip designers, like Apple (AAPL), AMD (AMD), and Nvidia (NVDA), as its customers. The reason for this is simple: it makes the most advanced semiconductor chips in the world, a lead so significant in the global economy that it finds itself as the major talking point when it comes to U.S.-China rivalry. It is this technological lead that has helped its stock more than double over the last twelve months, but I believe the potential is much bigger than this. The company’s financials do not paint a true picture of the business, and some recent developments merit a more qualitative approach to identifying the opportunity that this company presents.

A few days ago, you might have heard about TSMC raising the pricing on its 3nm process nodes by 15%. The move shows how the company enjoys pricing power and is willing to use that leverage to improve its revenue. Most of the impact of this move is likely to directly trickle down to the bottom line, improving the company’s earnings prospects. But the real consequences of this move will be seen somewhere else, and the market may not yet have woken up to that.

The developments around TSMC’s 2nm process nodes are worth looking at. The company entered high-volume manufacturing of this node in Q4 2025. The 2nm wafer is expected to be priced at $30,000, about 50% above the 3nm pricing. This is a massive tailwind for both revenue and margins. Apart from the pricing, the process node is progressing way better than the 3nm at a comparable stage. For instance, TSMC has already completed over 20 customer tapeouts with 70 more in the pipeline. For context, a tapeout is when the design is finalized, and the manufacturing can begin. This manufacturing is further supported by reliable customers. Apple alone has secured half the 2nm manufacturing capacity for its A20 chip, likely to be used in the iPhone 18. Other customers include Broadcom (AVGO), AMD, Intel (INTC), and Qualcomm (QCOM), among others.

The reason the above development is significant is that moving from one node to the next has historically been a tricky thing to execute. The customer concentration risk, when some customers may drop their plans for the prior node and instead opt for the latest one, can make it challenging to keep manufacturing at the same efficiency. The fact that TSMC can do that while raising prices on the previous node simultaneously shows it is not scared to move on; such is the nature of the artificial intelligence-induced demand these days!

About Taiwan Semi Stock

Taiwan Semiconductor Manufacturing Company is a leading global semiconductor company involved in the packaging, manufacturing, testing, and sale of ICs and other semiconductor devices. The company offers a wide range of wafer fabrication services used to produce different types of chips, including mixed-signal, embedded memory, complementary metal-oxide-semiconductor (CMOS) logic, radio frequency, and bipolar CMOS mixed-signal.

TSM stock has more than doubled over the past year, delivering gains of around 109%, while the iShares Semiconductor ETF (SOXX) returned about 165% over the same period. This shows that despite strong performance, TSM slightly underperformed the broader semiconductor sector. The trend has continued this year as well, with the stock rising approximately 41% while the index has generated twice the returns compared to the stock.

www.barchart.com

www.barchart.com

On the valuation front, TSM’s forward P/E of 26.25 may not seem to price in the unprecedented demand, but the same has been happening to Nvidia, which looks cheaper on a forward earnings basis despite the huge rally in the last couple of years. One fear is that the infrastructure buildup is unlikely to continue at the same pace. This shows in the consensus EPS growth estimates as well, where a 47% growth in 2026 reduces to 25% and 27.7% in 2027 and 2028, respectively. These are no doubt impressive growth numbers, but with AI development moving at a fast pace, investors seem hesitant to back 25% growth when other companies in the AI value chain are expected to grow at a much higher rate.

Taiwan Semi Posts Better-Than-Expected Earnings

The company reported its first-quarter fiscal 2026 earnings on April 16, beating both top-line and bottom-line estimates. Revenue for the quarter came in at $35.9 billion, comfortably exceeding consensus estimates by $410 million. This represents a 40.6% year-over-year (YoY) increase. Taiwan Semiconductor expects second-quarter revenue to range from $39 billion to $40.2 billion. This outlook reflects a 32% YoY and a 10% sequential increase at the midpoint. The company also raised its full-year 2026 revenue guidance and now forecasts revenue to grow by more than 30% in U.S. dollar terms. Meanwhile, it reaffirmed its commitment to steadily increasing shareholder dividends.

What Are Analysts Saying About TSM Stock?

Following the company’s earnings report, a few analysts updated their price targets and ratings on the stock, including Bank of America Securities and Barclays. On May 18, BofA reiterated a “Buy” rating and a $490 price target on the shares. Back on April 22, Barclays raised its price target on the stock from $450 to $470 while maintaining a “Buy” rating. This means that analysts are still divided when it comes to the price targets.

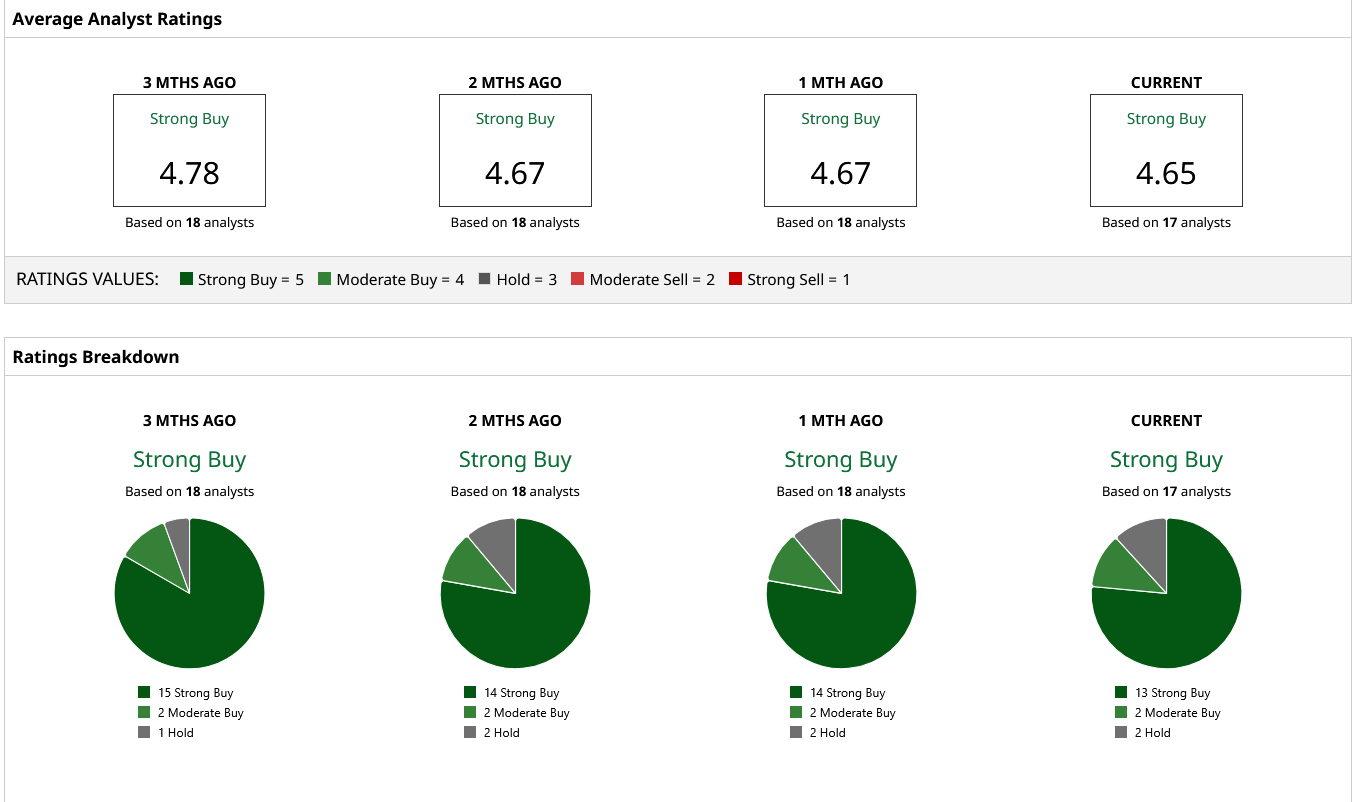

According to 17 Wall Street analysts covering TSM stock, it carries a consensus “Strong Buy” rating. Analysts assigned a mean price target of $450.46 to the stock. This reflects an upside of just over 8%, suggesting a lot of the demand is already priced in. What analysts may not yet have priced in is the impact of the 2nm node. Once that happens, the earnings growth will start looking attractive again.

www.barchart.com

www.barchart.com

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

This story was first published on Barchart

This week top market trends.

-

Taiwan Overtakes India as World's Fifth-Largest Stock Market

2026-05-26 :: stock :: bloomberg -

The bond market is sending a clear signal to the Fed

2026-05-26 :: treasuries & bonds :: yahoo finance -

Cloudflare stock plummets 23% amid AI-driven layoffs

2026-05-11 :: stock :: thestreet