Link copied

As Crude Oil Prices Whipsaw, Buy These 3 High-Yield Dividend Stocks Now.

investing ideas :: 9hrs ago :: source - barchart

By Ebube Jones

April WTI crude oil (CLJ26) spiked to $119.48 per barrel on Monday, the highest level for the nearest-futures contract in 3.75 years, before settling at $94.77 after Israel bombed 30 Iranian oil depots over the weekend. It now sits around $87 as of this writing.

The Strait of Hormuz, which handles about a fifth of the global oil supply, is now effectively closed, with Iran’s Revolutionary Guard Corps (IRGC) warning that vessels passing through "could be at risk from missiles or rogue drones."

The fallout has been swift across equities. On March 3, the S&P 500 ($SPX) fell to a three-month low, the Dow Jones Industrial Average ($DOWI) dropped to a two-month low, and the Nasdaq 100 ($IUXX) slid to a three-month low as higher energy costs added to inflation concerns.

For income-focused investors trying to stay steady through the volatility, the materials sector offers a useful pocket of opportunity. Three high-yield dividend stocks, Westlake Chemical Partners LP (WLKP), yielding 10.11%; Suncoke Energy (SXC), yielding 7.66%; and AngloGold Ashanti (AU), yielding 3.37%, stand out as reliable income plays in a market where visibility is challenging to find.

Each one has a low beta, ranging from 0.55 to 0.98, which means the shares have tended to move less sharply than the broader market. That is the kind of profile dividend investors look for when crude is above $100 and market volatility remains elevated.

But what makes these three names stand apart from the dozens of other materials stocks paying dividends right now, and can their yields hold up if the market volatility deepens? Let’s find out.

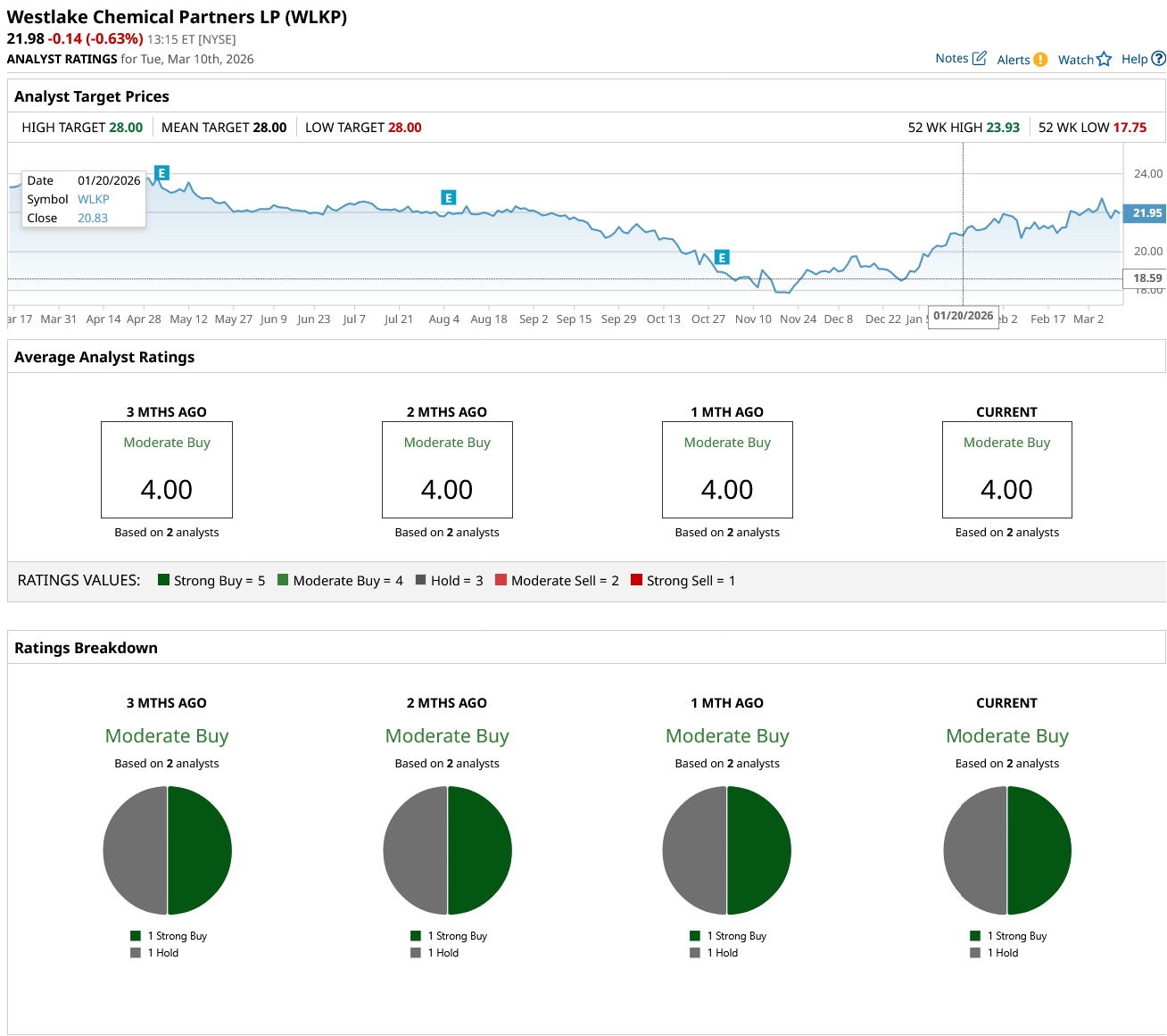

High-Yield Dividend Stock #1: Westlake Corporation (WLKP)

Westlake Chemical Partners LP is a master limited partnership that owns ethylene production assets and sells most of that output to Westlake Corporation (WLK) under a long-term agreement.

WLKP stock is still down 7.5% over the past 52 weeks, but it has gained 16% so far this year.

Valuation also still looks reasonable, with WLKP trading at about 12.26x forward earnings compared with roughly 15.51x for the sector.

That lower valuation stands out because investors are getting paid to wait, with a forward annual dividend of $1.89 per unit, an 8.69% yield, quarterly payouts, and a most recent distribution of $0.4714 declared in February. The main issue is that coverage is still tight, with a forward payout ratio of around 136%, so this is less a dividend growth story and more a case for dividend stability.

That stability showed up in the fourth-quarter numbers, where net income attributable to the partnership came in at $14.5 million, distributable cash flow was $18.8 million, and coverage improved to 1.13x. Full-year 2025 was weaker, with net income of $48.7 million and distributable cash flow of $53.4 million after the planned Petro 1 turnaround cut volumes and increased cash spending.

The more important development came earlier, when WLKP renewed its ethylene sales agreement with Westlake through December 2027, keeping in place the formula that supports a fixed $0.10-per-pound margin on 95% of output and has backed 46 straight quarterly distributions without a cut.

At the parent level, Westlake also completed the ACI/Perplastic acquisition in January 2026, expanding its specialty compounds business in Europe and North Africa and potentially increasing downstream demand across the broader Westlake system.

Analyst sentiment also remains positive, with the two analysts tracked giving the stock a "Moderate Buy" consensus and a $28 average target, implying roughly 28% upside.

www.barchart.com

www.barchart.com

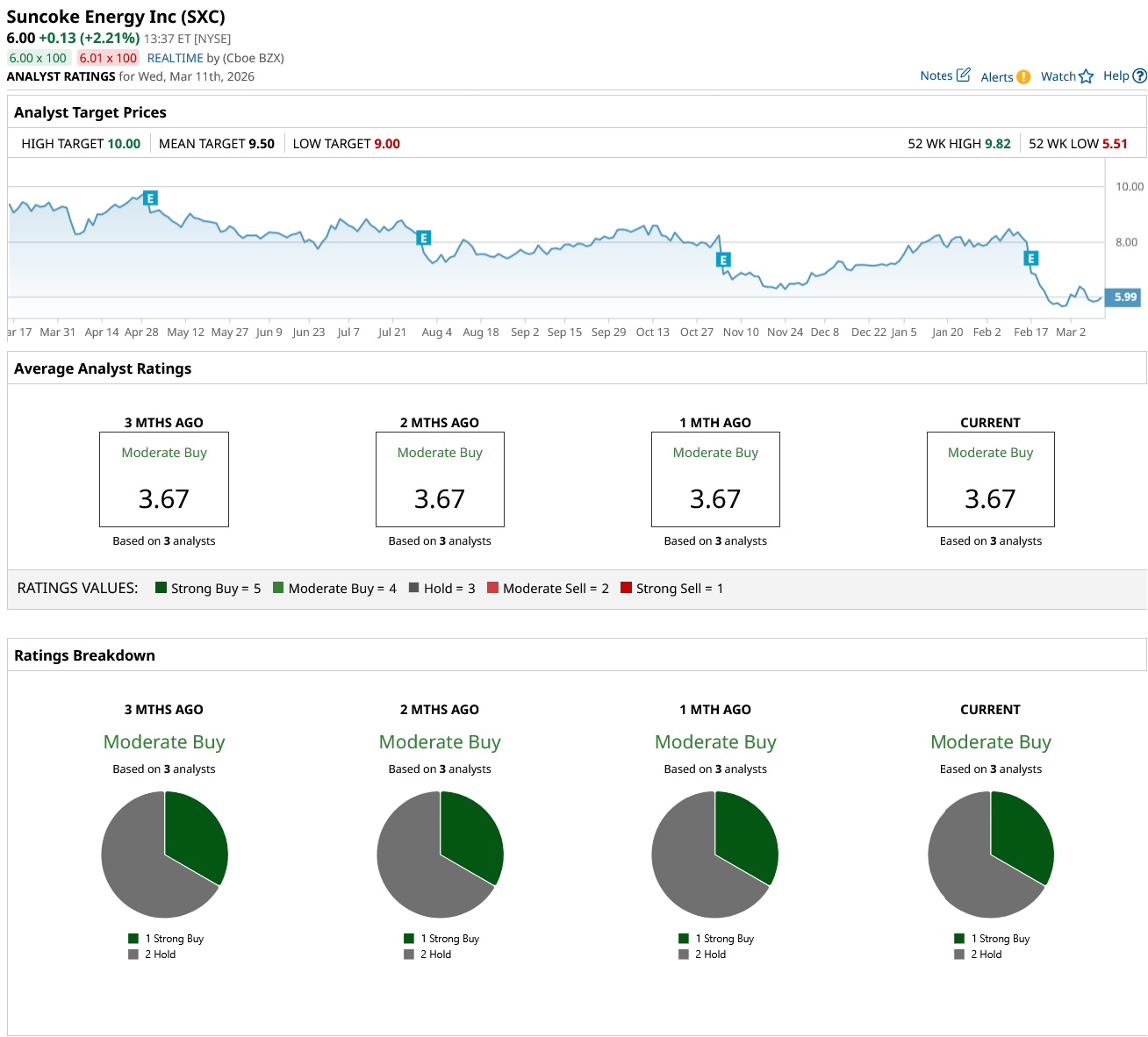

High-Yield Dividend Stock #2: SunCoke Energy (SXC)

SunCoke Energy is a metallurgical coke producer and industrial services company that supplies blast furnace and steelmaking customers under long-term contracts. That gives it direct exposure to heavy industry while also bringing in cash from logistics and mill services.

SXC stock has been under real pressure, falling 35% over the past 52 weeks and another 17% so far this year.

On valuation, SXC trades at about 15.68x forward earnings, which is roughly in line with the materials sector’s 15.51x. That suggests the market is not giving the stock much of a premium even with expectations for a recovery in 2026.

Investors are still getting paid well, with an annualized dividend of $0.48 per share, an 8.11% yield, quarterly payments, and a forward payout ratio near 79%, backed by a five-year streak of dividend increases.

Fourth-quarter results were weak on the surface, with a net loss of $85.6 million, or $1 per share, on $480.2 million in revenue, while full-year 2025 showed a $44.2 million loss on $1.84 billion in revenue. Management linked that softness to the Haverhill I closure, the Algoma contract breach, weaker Granite City economics, and mix changes, but it still guided for 2026 net income of $25 million to $43 million and about 3.4 million tons of domestic coke sales.

The bigger fundamental story is the company’s expansion. SunCoke closed its $325 million Phoenix Global acquisition in August 2025, adding electric arc furnace exposure and international markets, and it also extended its Granite City cokemaking agreement with U.S. Steel through December 2026, giving the business more contract visibility.

Analysts also remain constructive, with all three tracked rating the shares a consensus “Moderate Buy” and a $9.50 average target, implying roughly 58% upside.

www.barchart.com

www.barchart.com

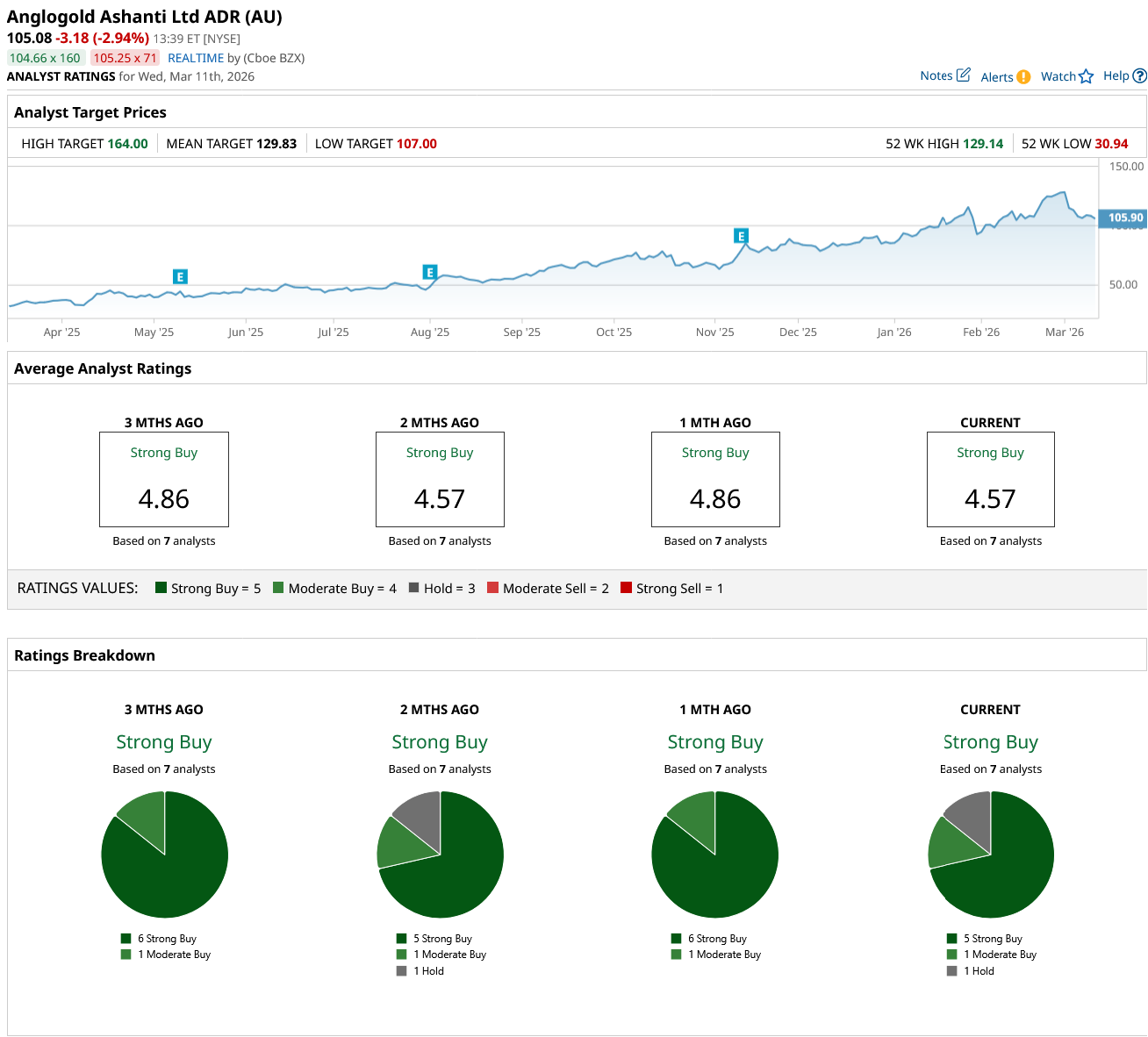

High-Yield Dividend Stock #3: AngloGold Ashanti Limited (AU)

AngloGold Ashanti is a global gold miner with producing assets, projects, and exploration exposure across multiple countries, so the model is simple: develop a broad mix of mines and use stronger gold prices to drive higher cash flow.

The stock already reflects that backdrop, jumping 230% over the past 52 weeks and another 24% year-to-date (YTD).

Even after that move, AU trades at about 11.64x forward earnings, below the materials sector average of 15.51x, which suggests the market still does not fully reflect its stronger earnings base and cash-generation profile. The payout is still competitive, with an annual dividend yield of roughly 2.37%, a forward payout ratio near 41.74%, quarterly distributions, and a most recent dividend of $0.91, giving investors both income and exposure to gold-price upside.

Fundamentals were very strong. Fourth-quarter profit reached $855 million, or $1.68 per share, on $3.07 billion in revenue, while full-year profit climbed to $2.64 billion, or $5.19 per share, on $9.73 billion in revenue. AngloGold also reported a record 2025 free cash flow of $2.9 billion and its highest-ever annual dividend payout, showing how much operating leverage improved as production increased and gold prices moved higher.

On the strategic side, the company completed its acquisition of Augusta Gold in October 2025, adding another U.S.-linked growth option to its portfolio.

Analysts remain firmly bullish, with all seven tracked rating the stock a consensus “Strong Buy” and a $129.83 average target, implying about 23% upside.

www.barchart.com

www.barchart.com

Conclusion

At the end of the day, these three names give income investors a rare mix of yield, defensiveness, and real assets at a time when crude's volatility can see it easily hit above $100, shaking everything from tech to Treasuries. WLKP and SXC look positioned to grind higher if cash flows normalize and management simply keeps the distributions coming, while AU already trades like a winner but still has some room if gold stays bid and execution holds. Of course, none of them are risk-free, but if oil remains elevated and volatility sticks around, the odds still favor their shares working higher over the medium term.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.Article sourced from Barchart

More News from Barchart

S&P Futures Gain as Oil Prices Retreat, U.S. PCE Inflation and GDP Data in Focus

As Crude Oil Prices Whipsaw, Buy These 3 High-Yield Dividend Stocks Now

Eon Resources Stock Jumps on Oil Hedging Announcement. Is High-Flying EONR a Buy Here?

Airbnb Stock Just Crashed Below Its 50-Day Moving Average. Should You Buy the Dip?

This week top market trends.

-

Trump’s 10% Levy Takes Effect as US Rebuilds Tariff Wall

2026-02-24 :: watchlist :: bloomberg -

Big European investors bet against swings in ECB, BoE interest-rate expectations

2026-03-11 :: stock :: reuters -

Netflix Drops Warner Bros. Bid, Leaving Paramount the Winner

2026-02-27 :: deals & business :: bloomberg

Recent global market news

-

Where Should You Put $10,000 Today? Look at These 3 Sectors That Are Winning While Tech Slumps.

2026-03-05 :: :: barchart -

Gold surges above $5,400 as demand for safe-haven asset jumps amid Iran conflict

2026-03-02 :: :: yahoo finance